Force Insight | Is Solana Going Down After FTX Collapse

The bankruptcy of FTX and Alameda Research has struck devastation on the crypto world, with lenders, exchanges, and funds all failing. The collapse has also wreaked havoc on markets, with the overall crypto market value plummeting 14 percent from $1.0T on November 6 (the day the FTX run started) to about $889B today.

Many individual tokens have dropped even more, with those owned by Alameda Research — notably Solana — taking the brunt of the damage. According to the now-infamous CoinDesk article on the trading firm’s balance sheet, Alameda controlled around $1.2 billion in SOL tokens on June 30.

While it’s uncertain how much of the latest drop was caused by Alameda or by traders’ concern, SOL fell from $35 to as low as $11 (68.5 percent) in the weeks after the FTX/Alameda collapse.

SOL, which was one of the best-performing tokens during the 2021 bull run, is currently roughly 95 percent below its all-time high. A catastrophe of this size would not only shock the trust of its most ardent followers, but it also has the ability to endanger its DeFi ecosystem and the network’s overall security.

This raises the issue… Is Solana dead? Will it ever recover?

Let’s look into the aftermath of the crisis and Solana’s future to see if we can find an answer.

Network Security and Stability

The native token of an L1 decreasing by 60% in 72 hours is a massive stress test. A crash of that magnitude not only threatens a chain’s DeFi ecosystem through mass-liquidations, which can saddle lending protocols with bad debt, but it also threatens stability and security by increasing the likelihood of an outage (a problem Solana has struggled with in the past) and decreasing the cost of network-level attacks.

Security

Following the FTX crash, Solana saw a large outflow of stakeholders. Since November 6, a net 54.6M SOL has been unstaked in the 9 epochs (which typically last 2–3 days), with the overall number of SOL staked declining 13.2 percent from 411.2M to 356.6M. This contributes to about 15% of the circulating supply of SOL.

During epoch 370, which lasted from November 7 to 10, a stunning 29.1M (53 percent of the net total) was unstaked. Unsurprisingly, the economic worth of the stake in safeguarding the network has dropped even more. Taking into consideration its price at the beginning of epoch 370 and the conclusion of epoch 378, the value of SOL securing the network has shrunk 65.3 percent from $14.7B to $5.1B.

This staking outflow might have been much greater if the Solana Foundation had not decided to postpone their intention to un-stake 28.5M SOL at the end of epoch 370 due to policy changes by Hertzner, a cloud service provider.

Despite these withdrawals, and maybe as a result of the 3–4 day latency before unstaked balances were liquid, Solana saw no security difficulties or large assaults. Given the departure of stakes, the L1 has the fourth biggest dollar-denominated stake and the 19th highest stake rate among PoS networks monitored by Staking Rewards.

Stability

Market volatility has an impact on network security and stability. This is because chains often witness an increase in blockspace demand during times of turbulence, putting a burden on validators as users and bots scramble to top-up collateral, complete liquidations, and catch other arbs produced by market dislocations.

Solana has a history of difficulty managing these surges, with multiple instances of poor service and outages. Since September 2021, the network has had four full failures, totaling 37 hours and 11 minutes of interruption.

The Solana community has been working on shipping solutions to boost liveliness, with changes such as stake-weighted QoS and QUIC already live on mainnet. Other enhancements, such as fee-markets and transaction size increases, are expected to be released in the following months.

These changes seem to be having an effect since Solana did not suffer any downtime or decreased performance during the crisis.

A blockchain is expected to be completely active, regardless of the circumstances. However, considering the network’s history and the gravity of the crisis, Solana’s performance throughout this era is noteworthy and an optimistic indicator that the network is becoming more robust.

Solana DeFi

Liquidity Crunch

Following the fall of the FTX, Solana faced a severe cash crisis.

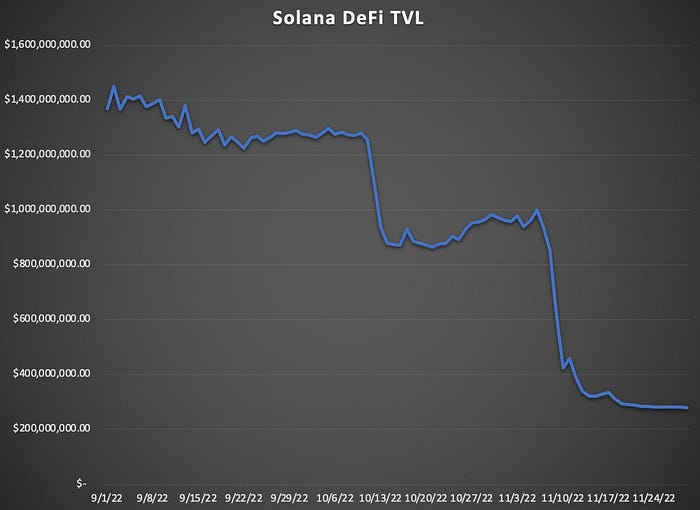

The network’s USD-denominated DeFi TVL has dropped 72.1 percent to $278.3M from $1.0B on November 6. This is understandable given the volatility of many of the assets placed into DeFi protocols such as SOL, ETH, and BTC. As a result, a decrease in TVL does not always imply that consumers are withdrawing cash from Solana DeFi.

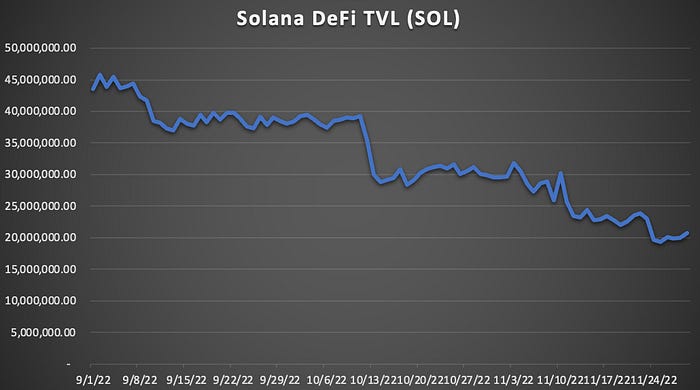

SOL-denominated TVL, on the other hand, has declined 27.5 percent from 27.2M to 19.7M since November 6. This suggests that the reduction in USD-denominated TVL may be due to consumers withdrawing their assets from DeFi rather than declining pricing.

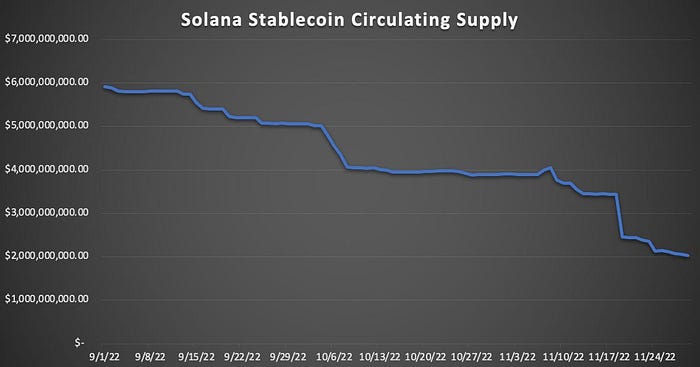

In recent weeks, the quantity of stablecoins on Solana has also shrunk dramatically.

Since November 6, the network’s stablecoin market price has fallen 46.1 percent, from $3.9 billion to $2.1 billion. This decline has been fueled in large part by a “chain-swap” by Tether, which moved $1 billion in supply from Solana to Ethereum on November 18. This transaction accounted for 55.5 percent of all stablecoin withdrawals since the crisis began.

Serum Wrecked

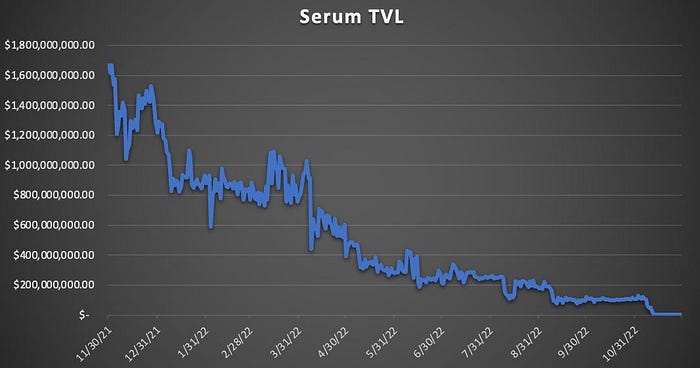

Many DeFi protocols have suffered greatly as a result of FTX, with projects with tight links to Alameda bearing the brunt of the damage. The most prominent is Serum, an order-book-based DEX whose governance token, SRM, has become the poster child for the “low-float, high FDV” token design, allowing the business to take out massive loans against the token at an inflated price.

Despite a 69.2 percent price decrease over the last three and a half weeks, SRM still trades at a $2.4B FDV. Serum was also a basic component in Solana DeFi, with protocols such as Raydium, Zeta Markets, PsyOptions, and others constructed on top of it. This would not have been a problem if Serum’s contracts had been immutable since the protocol would have continued to operate despite the failure of its governance token. Serum’s contracts, on the other hand, are governed by admin keys owned by FTX. This placed the Serum and, by extension, the Solana ecosystem at jeopardy, since a Serum hard-rug might cause catastrophic spread.

Yet, despite the TVL in Serum plummeting 99.6 percent from $121.7M pre-crisis to $434K, with Raydium delaying market-making on the DEX and Zeta Options suspending deposits, this issue has been mostly averted.

The Solana DeFi community has also launched OpenBook, a Serum fork that has raised $1.5 million in TVL. It remains to be seen if the fork will survive, but it may provide a temporary answer for Serum-based enterprises as a lower-risk liquidity venue than its parent protocol.

Down, But Not Out

As we can see, Solana is in pain, yet he is not dead. Though Solana’s pricing is considerably closer to the $3 figure from SBF’s notorious tweet than it was a few weeks ago, the network’s robustness has been superb, with no outage or decreased service throughout an intense volatility event. So far, the chain has also endured a substantial amount of it being taken down.

While this is more of a matter of the blockchain matching expectations than any great feat, it is noteworthy considering Solana’s history of insecurity and outages. Operating without hitch during this turbulent period should help the network gain greater trust in the future.

But it doesn’t mean things will be easy for Solana in a short term. Solana DeFi has taken a huge hit, with massive cash withdrawals, notably from projects with links to FTX and Alameda, such as Serum. It will also take time for the blockchain to be free of the odor of FTX, which many considered as an important ally for the network. Furthermore, it is uncertain how much SOL Alameda currently has; they will almost probably liquidate whatever remains on their books throughout the procedures.

Concerns about Solana’s long-term technological competitiveness linger since they will almost certainly have to adopt modularity rather than cling to a monolithic design. It’s worth asking whether developers and community members who haven’t seen a 95%+ decline previously will remain around in the next months and years.

Having stated that, crypto natives understand that Solana is more than simply an SBF pet project, and have seen usage remain stable even throughout the down market. The most recent blockchain hackathon had 750 applications, and SOL-denominated NFT volume is up 102 percent M/M, crisis be damned.

In the long term, the loss of the FTX and Alameda complex may be addition by subtraction, since the ecosystem will no longer be vulnerable to their unscrupulous business tactics and token designs. As a consequence, Solana may become more decentralized and equal.

So. Yes. Solana is in a horrible way. There’s no denying it. However, claims of its demise have been largely overstated to date.

Learn more about Force Community